February 2026 saw the convergence of two seemingly unrelated threads. One was technological: an artificial intelligence project named OPEN by the U.S. Defense Advanced Research Projects Agency (DARPA) was being transferred to a nonprofit organization. Its core function is to generate structural prices for strategic commodities such as germanium, gallium, antimony, and tungsten that lack exchange-based pricing. The other was policy: the Trump administration was building FORGE (Forum on Resource Geopolitics and Economic Security), a critical minerals trade bloc covering more than 50 countries, paired with adjustable tariffs and a $120 billion strategic mineral reserve plan. Washington plans to embed the AI-generated prices from the former into the institutional framework of the latter: using AI models to calculate what strategic commodities should be worth, then using tariffs and allied procurement to make this price a market reality.

If this vision comes to fruition, it will mark the first time artificial intelligence has been systematically integrated into national pricing capacity-building, elevating price discovery—a function once left to spontaneous market forces—into a national security toolbox. It is both an institutional response to China's export controls and a critical step for the U.S. in translating its AI technological advantages into economic governance power: an upgrade from subsidizing supply to building pricing institutions with AI. Yet while AI can compute the theoretical cost of a metal, it cannot conjure up refining capacity out of thin air, resolve allied divisions, or circumvent the constraints of WTO rules.

This article dissects the internal logic and structural vulnerabilities of the U.S.'s AI-enabled strategic commodity pricing system across three dimensions: AI technical mechanisms, institutional design, and geoeconomic impact. It also assesses its potential ramifications for the global commodity governance paradigm and the artificial intelligence governance agenda.

01 The Pricing Vacuum in Strategic Commodities and the AI Intervention Opportunity

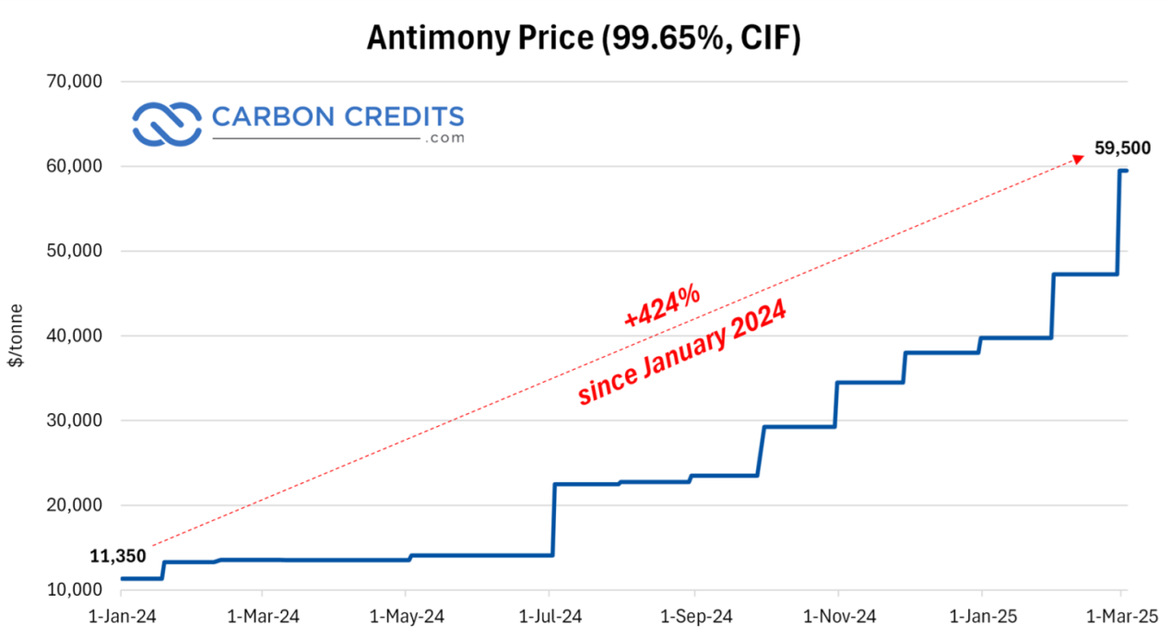

In February 2026, a metal called antimony tested the limits of the global commodity market's understanding. Widely used in military ammunition hardening and flame-retardant materials, antimony experienced an unprecedented price surge following China's implementation of export licensing controls in September 2024. Rotterdam prices for the metal rose from approximately $13,000 per ton in early 2024 to $57,000–$60,000 per ton by mid-2025—a surge of over 400%. Meanwhile, domestic prices in China remained in the $25,000–$30,000 range, creating a twofold price gap for the same metal on opposite sides of the globe.

Recent Volatile Price Movements of Antimony

Source: S&P Global

What troubles Western buyers most is that they cannot even determine which price is closer to the true cost: antimony is not listed on the London Metal Exchange (LME), has no standardized futures contracts, and global trade relies primarily on bilateral over-the-counter (OTC) contracts and quotes from a handful of price reporting agencies (PRAs) such as Fastmarkets. A June 2025 advisory report by the U.S. Commodity Futures Trading Commission (CFTC) bluntly stated that many critical minerals markets lack exchanges and that their price integrity is compromised by the absence of governing bodies. This predicament of thinly traded markets—characterized by extremely low trading volumes and severe liquidity shortages—is not unique to antimony; germanium, gallium, and tungsten face the same issue.

It is in this wasteland of near-failed price signals that Washington seeks to rebuild a pricing order centered on artificial intelligence: an AI-generated reference price embedded within a trade bloc framework covering over 50 countries, backed by adjustable tariffs as an enforcement mechanism. If realized, this would mark the first systematic use of artificial intelligence to build national-level strategic commodity pricing capabilities.

Why has the U.S. taken this step? On the surface, it is a reactive response to China's export controls; at its core, however, lies a structural dilemma. Since the controls were introduced, U.S. antimony prices have risen by over 400%, tungsten benchmark prices surged from $335–$345 per tonne unit in January 2025 to $1,050–$1,115 in December—a 218% increase—and Rotterdam gallium prices rose by over 150% compared to pre-control levels.

Yet high prices alone have failed to attract alternative supply. Gracelin Baskaran, a researcher at the Center for Strategic and International Studies (CSIS), documented a key phenomenon: the share price of MP Materials, the U.S.'s only rare earth mining company, rose far more following the announcement of price guarantee policies than it did when the government provided billions in financing. This indicates that the market views price predictability as scarcer than capital itself. This realization has driven policy evolution from supply-side subsidies to a systemic institutional arrangement: simply pouring money into mining is insufficient; investors must be assured that mineral prices will not collapse once China resumes exports.

02 The AI Technical Toolbox: A Strategic Pricing Engine

To address the pricing challenges facing critical minerals, the U.S. Defense Advanced Research Projects Agency (DARPA) launched the OPEN program in 2023: Open Price Exploration for National Security. Managed by Jonathan Doyle, program manager at the Strategic Technology Office, and conducted in partnership with the U.S. Geological Survey (USGS), the initiative was not originally designed to directly generate transaction prices. In Doyle's words, the program aims to solve a decades-long problem of information asymmetry.

OPEN's technical approach is organized along two tracks:TA 1 focuses on cost estimation and structural pricing, led by supply chain risk analytics firm Exiger and S&P Global Commodity Insights. Its core logic breaks down mineral prices into four components:input costs—including labor, energy, reagents, transportation, processing, and capital expenditures—supply and demand shocks, non-competitive distortions, and random volatility. Anchored on observable production costs, it estimates a theoretical price stripped of distortions, known as the structural price.

TA-2 concentrates on supply and demand forecasting, carried out by Charles River Analytics in collaboration with Finnish mining data firm Rovjok, GE Research, and S&P Global. It uses artificial intelligence and economic modeling to generate geographically and temporally indexed probabilistic supply and demand projections. The model has reportedly integrated more than 70 mining-related datasets, drawing from financial data provider FactSet, Benchmark Mineral Intelligence, the U.S. Department of Commerce, and other sources.

In short, OPEN has built an AI-driven technical toolkit for strategic commodity pricing: it uses machine learning to decompose cost structures and artificial intelligence to forecast supply and demand dynamics, seeking to deliver computational price signals for strategic minerals that lack high-frequency exchange-based pricing.

As a technical product, however, OPEN has clear limits to its capabilities, two of which directly affect the credibility of its outputs.The first lies on the input side: OPEN targets precisely the least traded and most data-sparse commodities, meaning the model's maximum accuracy is fundamentally constrained by the quality and coverage of input data. This creates a data paradox: the markets most in need of reference prices are the ones that lack the data required to train reliable models.

The second lies on the output side: for reference prices to be adopted commercially, market participants must be able to understand and verify the underlying calculation logic—a requirement inherently at odds with the black box nature of closed source AI models. The view of Ian Lange, an economist at the Colorado School of Mines, is representative: he argues that using machine learning to forecast mineral prices is worthless, much like attempts to reliably predict oil prices using similar methods.

Notably, a third, still latent risk exists: adversarial manipulation of AI pricing models—a common challenge when artificial intelligence is embedded in high stakes governance settings. When OPEN functioned only as an internal analytical tool for the Pentagon, incentives for external interference were limited. But once its AI outputs are used as triggers for tariffs or benchmarks for contract pricing, suppliers with market dominance gain strong incentives for strategic interference: adjusting export data, manipulating domestic price signals, and selectively disclosing production figures can all systematically distort model outputs.

In other words, OPEN faces not merely a passive computational challenge, but a human machine dynamic that intensifies as the AI becomes more institutionalized—exposing the core vulnerability of AI systems as they transition from technical tools to governance infrastructure.

For OPEN to move from a Pentagon laboratory to policy implementation, a critical organizational transition was required.According to a Reuters report in May 2025, OPEN's artificial intelligence models are being transferred to the Critical Minerals Forum (CMF), a non profit organization, for operation. The Pentagon will provide funding through at least 2029 and plans to transfer intellectual property to CMF around early 2027.

CMF has branded OPEN's output as the Resilient Price, defined as the true cost of compliant metal production without state subsidies.This quasi public good arrangement—developed by the military, operated by a non profit, and used by both industry and government—provides an organizational foundation for embedding the reference price into formal systems, while maintaining necessary distance from the Pentagon. If the reference price were issued directly by the Department of Defense, its acceptability in commercial contracts and under international trade rules would be severely diminished.

The Critical Minerals Forum is an independent 501(c)(6) nonprofit business trade association funded by the Defense Advanced Research Projects Agency (DARPA). It brings together critical minerals miners, processors, end user manufacturers, investors, and public sector entities.

Source: Critical Minerals Forum

Yet Washington’s ambitions for the OPEN program extend far beyond market transparency. Three sources familiar with the matter confirmed to Reuters that the Trump administration plans to embed OPEN’s reference price outputs into the framework of the Forum on Resource Geostrategic Engagement (FORGE), a trade bloc it is assembling.

On February 4, 2026, Vice President JD Vance, speaking at a critical minerals ministerial meeting chaired by Secretary of State Marco Rubio and attended by 55 nations, proposed that alliance members establish reference prices for critical minerals “at every stage of production,” paired with “adjustable tariffs to safeguard price integrity.” Vance declared the global critical minerals system “is failing,” arguing that repeated price collapses have left new mining projects “stillborn.”

U.S. Vice President JD Vance delivers remarks at the Critical Minerals Ministerial held at the U.S. Department of State in Washington, D.C., on February 4, 2026.

Source: Reuters

The implicit assumption behind this system is that as long as the AI-generated reference price is sufficiently credible and tariff guardrails robust enough, market participants will spontaneously organize transactions around the reference price, eventually turning it into a self-fulfilling price benchmark. Yet every link in this chain carries the risk of breakdown.

At the implementation level, transshipment represents the most direct circumvention method. Reports indicate that between December 2024 and April 2025, the United States imported more than 3,834 metric tons of antimony trioxide from Thailand and Mexico—several times the total imports over the previous three years. Some shipments were misclassified as “zinc, iron, or art supplies.”

According to research by the Stimson Center, China’s germanium exports to Belgium surged **224% in 2024, roughly offsetting the decline in exports to the U.S.

From the U.S. perspective, this mirrors the enforcement challenges seen with the Russian oil price cap. Analysis by the Center for Strategic and International Studies (CSIS) shows that “shadow fleets,” document fraud, and buyer redirection have systematically eroded the effectiveness of price cap mechanisms.

03 Governance Spillover of AI Reference Pricing: From Mineral Pricing to a New Paradigm for Strategic Commodities

Once a U.S.-led critical minerals reference price regime takes shape, its spillover effects will extend far beyond the minerals sector. The most direct impact will be felt at both ends of the industrial chain. For upstream producers, a credible price floor could reshape financing logic for Western mining projects: shifting from “highly uncertain price cycles, making project financing difficult” to “institutional price anchors that enable cash flow modeling based on reference prices.”

For downstream industries, however, reference prices will be systematically higher than current market levels, because the definition of a “Resilient Price” inherently excludes low-cost production that relies on state subsidies. This cost increase will inevitably pass through to manufacturing sectors including automotive, electronics, and defense. The Peterson Institute for International Economics (PIIE) has warned that the regime faces “untested WTO risks and enormous implementation complexity.” A deeper tension stems from structural divergences among allies: resource-exporting nations prefer higher mineral prices and opportunities to develop processing industries; manufacturing powers favor the lowest possible input costs; while the U.S. seeks to secure both supply security and price stability.

Cullen Hendrix of the Peterson Institute summarizes this as a “trilemma of bankability”: capital markets demand high returns, manufacturers demand low prices, and national security demands low risk—three inherently conflicting goals. Notably, nearly all U.S. critical minerals stocks fell on the day of the February 4 ministerial meeting: MP Materials dropped more than 8%, and USA Rare Earth fell 10.8%. This suggests market skepticism over government-managed pricing extends far beyond academic debate.

The impact of the reference price regime on existing pricing mechanisms also deserves attention. Today, critical minerals price signals are provided mainly by two types of institutions: first, price reporting agencies (PRAs) such as Fastmarkets and Argus Media, which generate benchmark assessments by collecting over-the-counter transaction data and market surveys; second, exchanges—the Chicago Mercantile Exchange (CME) is developing rare earth futures contracts, and the London Metal Exchange (LME) is evaluating the inclusion of more minor metals in its trading system.

OPEN’s reference prices have a complex, competitive yet complementary relationship with these existing mechanisms. If the AI-driven methodology behind reference prices is sufficiently transparent and widely adopted by the market, it could push price reporting agencies to improve data coverage and methodological transparency, creating healthy competition. However, if reference prices gain influence primarily through tariff guardrails and “AI technological hegemony” rather than voluntary market acceptance, they risk creating a distortion: market participants trade around AI reference prices within compliance frameworks, while actual supply and demand determine prices outside them, forming a dual-track price system. The experience with the Russian oil price cap shows that once such a dual-track structure emerges, the gap between compliant and market prices becomes a breeding ground for arbitrage and circumvention.

For the U.S.-China strategic competition cycle, the institutionalization of the reference price regime could redefine the strategic space for both sides. From Washington’s perspective, if reference prices are successfully embedded in the FORGE framework and adopted by allies, the price shock effects of China’s export controls will be institutionally absorbed. Western firms will no longer base investment decisions on volatile spot prices, but on long-term contracts anchored to reference prices for capacity planning. As a result, China’s strategic leverage of “using controls for bargaining chips” will be blunted.

February 24, 2026: Assistant Secretary of Defense for Industrial Base Policy Cadena II testifies before the Senate Armed Services Committee that ensuring resilient and reliable supply chains for critical minerals is vital to national security and the economy.

Source: U.S. Department of Defense

Yet this logic depends entirely on genuine physical production capacity backing the reference price. If alternative Western refining and processing capacity fails to materialize in time, the reference price risks becoming little more than a political construct floating above real-world supply. Tariff guardrails can prop up prices on paper, but they cannot conjure germanium ingots or gallium ingots out of thin air.

A commentary from Rare Earth Exchanges puts it succinctly: pricing power follows physical control. Without substantial expansion of refining capacity outside China, the AI benchmark risks being a framework erected atop an unchanged supply reality.

Whether this condition is met or not, a Western trade bloc anchored on AI-determined prices will almost certainly accelerate an upward spiral of “controls, countermeasures, alternative supply development, and further controls.” The difference lies in the direction: an AI reference price supported by real capacity will push competition toward supply chain restructuring, while one lacking physical backing could amplify market chaos and create openings for adversaries to counteract. This is the fundamental paradox of AI as a governance tool: algorithms can optimize information processing, but they cannot replace physical-world capacity building.

One often-overlooked yet profoundly significant impact on global AI governance is the precedent effect. If the AI-driven critical minerals reference price regime proves successful – or even achieves adoption for government procurement of just germanium and antimony – it will almost certainly be replicated in other strategic commodity sectors characterized by thin trading, high concentration, and strong geopolitical sensitivity. These include rare earth permanent magnets, high-purity spherical graphite, natural uranium, semiconductor-grade polysilicon, and select critical biopharmaceutical raw materials.

Once the model of “state-led AI reference prices, tariff guardrails, and allied procurement” becomes a replicable policy template, the fundamental paradigm of global commodity governance will shift from “market pricing, government regulation” to “AI pricing, government endorsement, market adaptation.” This means artificial intelligence is no longer merely a tool for industrial efficiency, but is emerging as power infrastructure in international economic governance.

In its public comment request opened on February 26, 2026, the Office of the United States Trade Representative (USTR) explicitly expanded the scope from the initial four minerals to “other critical minerals and processed materials potentially eligible for the reference price mechanism.”

For China, which acts as both a major supplier and consumer at critical nodes of strategic supply chains, the success or failure of this AI-enabled institutional template will shape not just the trading terms of specific minerals, but the trajectory of the fundamental questions in international economic governance over the next decade: who sets prices, by what algorithms, and who controls AI pricing power. It thus becomes an unavoidable new issue on the global artificial intelligence governance agenda.

Author

Li Yaqi, Research Assistant of CGAIG