The issue of power supply for artificial intelligence (AI) has emerged as a global focal point of attention. At the World Economic Forum in Davos in January 2026, Elon Musk stated that power has become the ultimate bottleneck for AI deployment. While chip production capacity is expanding exponentially, the development of power infrastructure has fallen far behind such growth momentum. To alleviate power supply pressure, he has promoted the construction of independent power generation facilities by xAI, his AI enterprise, and proposed deploying space-based solar-powered data centers. Ruth Porat, President and Chief Investment Officer of Alphabet (Google’s parent company), also pointed out that insufficient investment has been made in power grids over the past two decades, and shortages in grid access and critical power equipment have become physical constraints on AI development.

In March of the same year, French President Emmanuel Macron emphasized at the World Nuclear Energy Summit in Paris that leveraging its strengths in nuclear power, France is fully capable of independently constructing data centers and computing power infrastructure to leverage nuclear leadership for AI sovereignty. These remarks demonstrate that international competition surrounding artificial intelligence is no longer merely a technological rivalry over algorithms and chips; it has increasingly evolved into a contest centered on power infrastructure.

On March 10, 2026, at the World Nuclear Energy Summit in Paris, Emmanuel Macron explicitly voiced his support for nuclear energy development to meet the surging power demand amid the AI era.

Image source: Abdul Saboor / Reuters

Europe occupies a complex position in this contest. The region is not lacking in political will to advance artificial intelligence: in recent years, the European Union and its major member states have set ambitious targets for the development of computing power infrastructure, aiming to strengthen international competitiveness and reduce reliance on external cloud services and computing systems. Nevertheless, the power foundation underpinning such ambitions remains far from robust. Unlike the United States’ flexible power procurement landscapeor China’s unparalleled speed in scaling generation and transmission infrastructure, Europe lacks the robust power foundation necessary to underpin its strategic AI ambitions. This disconnect between ambition and physical reality makes power supply a critical lens for assessing the trajectory of Europe’s AI industry.

Against this backdrop, this paper seeks to address the following questions: What impacts has AI development exerted on global power supply? What power bottlenecks hinder AI expansion across Europe? What policy approaches have EU institutions and member states adopted to alleviate power supply pressures? Constrained by power availability, what development prospects lie ahead for Europe’s AI sector?

01 The Power Anchor of Global Computing Competition

AI model training and inference are highly energy-intensive, with such dependency intensifying amid accelerated model iteration. Training involves iterative computation and parameter adjustment across massive datasets, typically requiring large-scale high-performance computing clusters to operate continuously for weeks or even months. According to MIT Technology Review, a single training run for GPT-4 consumes approximately 50 gigawatt-hours of electricity—roughly equivalent to powering the entire city of San Francisco for three days. Each new generation of models features larger parameter scales and richer multimodal capabilities, driving further rises in training energy consumption and making model iteration itself a key driver of growing power demand. Inference refers to the process whereby models generate responses to user queries. While single inference operations consume less electricity than training, the widespread integration of AI into high-frequency scenarios such as search engines, office software, coding, and content creation has led to surging inference volumes, resulting in substantial cumulative energy use. Deloitte reports indicate that inference accounted for 50 percent of total AI computing power consumption in 2025, with the figure projected to rise to roughly two-thirds by 2026. Meanwhile, supporting systems essential for sustaining high-density computing—including cooling facilities, power conversion units, and backup power supplies—also consume vast quantities of electricity on an ongoing basis.

Data centers constitute the physical infrastructure supporting AI operations. Driven by overlapping demands as outlined above, global electricity consumption by data centers has already reached considerable levels, with its share of overall global power use set to keep expanding. According to estimates by the International Energy Agency (IEA), global data center power consumption stood at approximately 415 terawatt-hours in 2024, representing 1.5 percent of total worldwide electricity demand. Though this proportion appears modest, the absolute volume is substantial: a typical AI data center consumes roughly as much electricity as 100,000 households, while the largest projects currently under construction reach 20 times this scale. The IEA further forecasts that global data center power usage will double to around 945 terawatt-hours by 2030—slightly exceeding Japan’s entire current national electricity consumption—and climb further to approximately 1,200 terawatt-hours by 2035. Geographically, this growth is heavily concentrated within a small number of major economies: the United States accounts for around 45 percent of global data center power consumption, China approximately 25 percent, and Europe about 15 percent. By 2030, data centers will contribute over 20 percent of incremental power demand across advanced economies. In the United States, electricity allocated to data centers will surpass the combined power consumption of all energy-intensive manufacturing sectors, including aluminum, steel, cement, and chemicals.

As demand expands rapidly, power supply has emerged as a tangible bottleneck constraining the expansion of the AI industry. The IEA estimates that without effective mitigation of power-related risks, approximately 20 percent of planned data center projects may face delays. In 2025, newly added data center capacity across Europe, the Middle East and Africa declined by 11 percent year-on-year, largely attributable to constrained power availability. Faced with such limitations, major technology corporations are no longer reliant solely on grid-purchased electricity to meet their needs; instead, they have begun direct engagement in power generation and grid dispatch. Microsoft has signed agreements to recommission Unit 1 of the Three Mile Island Nuclear Generating Station in Pennsylvania, Amazon procures power from the Susquehanna Nuclear Power Plant in the same state, while Google plans to deploy advanced nuclear energy solutions and has entered demand-response agreements with utility providers.

The Three Mile Island Nuclear Generating Station boasts a history spanning over five decades. Unit 2 was permanently shut down following a severe accident in 1979, while Unit 1 ceased operations in 2019. Today, driven by the surging power demand fueled by AI data centers, the long-idled Unit 1 is scheduled to restart in 2027.

Image source: U.S. Department of Energy

Power-related factors are also reshaping the investment structure of the AI industry. According to McKinsey estimates, global capital expenditure on data center infrastructure is projected to exceed 1.7 trillion U.S. dollars by 2030. Of this sum, approximately 1.3 trillion U.S. dollars will be allocated to power infrastructure including power plants, transmission lines, transformers and generators, accounting for over three-quarters of total infrastructure investment. In other words, a substantial proportion of future capital spending in the AI industry will not go toward chips and servers, but toward securing a stable power supply for such equipment. Beyond serving as a fundamental physical prerequisite for AI operations, power has evolved into a critical variable shaping the competitive landscape and geographical distribution of the AI sector.

02 Europe’s Power Bottlenecks in AI Development: Three Mismatches and Two Major Barriers

At present, the primary constraint hindering Europe’s AI advancement lies in the fact that the expansion of Europe’s power gridis struggling to keep pace with the exponential surge in compute demand. Ireland serves as a typical case in point. Home to the EU headquarters of major U.S. tech giants and one of the EU’s core clusters for data centers, the country had approximately 5.8 billion euros worth of data center projects on hold by the end of 2025. Though these projects had secured land rights and construction permits, insufficient grid capacity prevented them from connecting to the power supply. In the long run, Europe’s share in the global data center market has continued to decline, dropping from over 25% in 2015 to 15% in 2024, with its growth rate over the past decade standing at merely half the global average. Persistent power bottlenecks risk pushing Europe further behind in the development of AI computing power infrastructure.

First is the temporal mismatch, marked by planning silos between digital infrastructure and power systems. Power infrastructure entails far longer construction cycles than data centers. While large-scale data centers in Europe can generally be completed within two years, lengthy queues for grid connection have extended their actual delivery cycles to nearly four years on average. In the five major European data center hubs—Frankfurt, London, Amsterdam, Paris and Dublin, collectively abbreviated as FLAP-D in the industry—the average waiting period for power connection ranges from seven to ten years, with some projects facing waits of up to thirteen years. Inefficiencies also plague the queuing mechanism itself. In Italy, for instance, the pending grid connection capacity for data centers reached 30 gigawatts by the end of 2024, equivalent to roughly 40% of the country’s peak power load. Nearly 80% of these applications were submitted within the preceding twelve months, including speculative proposals unlikely to be implemented, which further exacerbates grid application congestion.

Second is the spatial mismatch, characterized by prominent geographical imbalances between power supply and demand. At the urban level, the FLAP-D hubs concentrate around 62% of Europe’s total data center capacity. Among these cities, only Paris maintains relatively ample grid carrying capacity and can sustain steady investment inflows. Grid operators in regions covering Dublin, Amsterdam and Frankfurt have imposed restrictive measures, effectively halting new data center connections. London is also grappling with worsening grid congestion and prolonged connection waiting times. At the national level, data centers already consume about 22% of Ireland’s total electricity, a figure expected to rise to 32% by 2026. As data center loads keep climbing, Ireland faces heightened risks of power shortages during winter peak periods. The Netherlands presents an equally noteworthy scenario: its data centers are predominantly clustered in North Holland, where Amsterdam is located. The provincial government introduced stringent regulations on new and expanded large-scale data centers in 2022, followed by tighter national oversight on site selection and energy consumption, in an effort to strike a balance between industrial development and grid capacity limits.

This image depicts Google’s data center located in Dublin, Ireland. Boasting a common law system, linguistic advantages and a low-tax regime, Ireland has emerged as the primary gateway for major U.S. technology firms entering the EU market. Dublin currently ranks as the world’s third-largest and Europe’s largest hyperscale data center hub; nevertheless, the rapid expansion of data centers has imposed severe pressure on local power supply capacity.

Image source: Google Dublin Data Center

Thirdly lies the structural mismatch, manifested in inadequate flexibility of the power grid system and substantial shortfalls in cross-border electricity transmission. AI data centers require reliable, long-duration continuous power supply. Yet Europe’s power mix is undergoing a rapid transition toward intermittent renewable energy sources such as wind and solar power. By 2030, renewables and nuclear energy are projected to supply approximately 85% of electricity for European data centers. While intermittent power sources can support stable loads in theory, they rely on energy storage, demand-side response mechanisms and efficient cross-border dispatch—areas where Europe still faces notable deficiencies. According to the 2025 monitoring report published by the Agency for the Cooperation of Energy Regulators (ACER), remedial measures, specifically re-dispatching and countertrading, to manage grid congestion adopted by EU transmission system operators to mitigate congestion incurred costs of 4.3 billion euros in 2024, covering around 60 terawatt-hours of electricity—equivalent to Austria’s total annual power consumption. In core central European regions, the average physical capacity actually available for cross-border transmission on the most congested power lines stands at merely 54%, well below the 70% mandated by EU legislation. Furthermore, over 60% of major transmission infrastructure projects are subject to delays. This indicates that even where ample clean power is available in certain regions, it cannot always be delivered to data center sites at low cost. Insufficient system flexibility and constrained cross-border transmission will ultimately translate into higher electricity expenses and heightened power supply risks.

In addition, two systemic barriers stymie Europe’s strategic ambitions.

The first concerns ageing grid infrastructure. The An EU Action Plan for Grids, issued by the European Commission in 2023, highlights that roughly 40% of the EU’s distribution networks have been operational for more than four decades, requiring grid investment of up to 584 billion euros throughout the current decade. Designed primarily to serve large centralized power stations and relatively stable end-user loads, these ageing facilities struggle to accommodate emerging demands such as renewable energy integration, industrial electrification and the expansion of data centers. Consequently, future grid investment cannot be fully allocated to accommodate new computing loads; a considerable portion must first cover asset replacement and the reinforcement of vulnerable network segments.

The second barrier involves elevated power and computing costs. Electricity expenditure accounts for a substantial share of data center operational costs, with power prices directly determining long-term project expenses and investment returns. IEA statistics indicate that in 2025, average electricity prices for energy-intensive industries within the EU remained more than twice those in the United States and nearly 50% higher than in China. Meanwhile, volatility in European power markets has intensified. In the first half of 2025, driven by surging natural gas prices and rising carbon allowance costs, wholesale electricity prices across the EU rose by approximately 30% year-on-year. Conversely, periods with abundant wind and solar generation create temporary power surpluses, pushing negative electricity prices to occur for around 6% of operational hours in markets including France, Germany, the Netherlands and Spain. In short, Europe’s power market is characterized by alternating peaks of high prices and negative pricing. For data centers requiring uninterrupted round-the-clock operation, greater price volatility complicates cost forecasting and long-term power procurement arrangements. Persistent cost disadvantages not only inflate operational expenditure for onshore computing deployment within Europe but also incentivize European enterprises to rely more heavily on cross-border external cloud resources—contradicting the EU’s policy emphasis on technological autonomy and domestic computing infrastructure development.

03 Policy Pathways for Europe to Alleviate Power Supply Pressures on AI Development

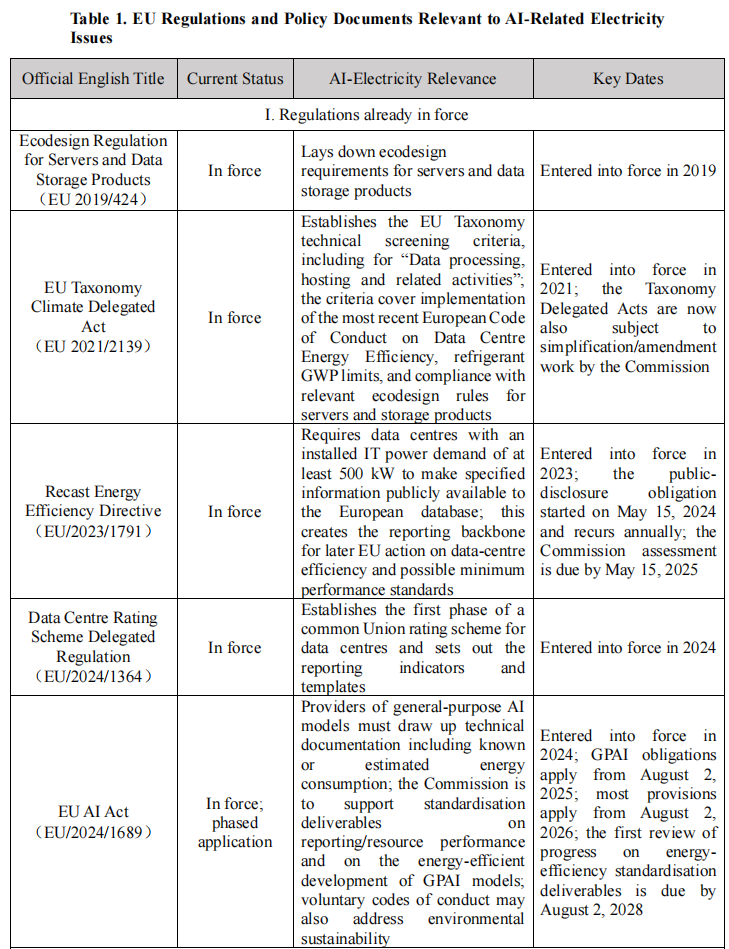

Faced with power-related bottlenecks constraining AI expansion, EU institutions and member states have introduced a raft of targeted policies starting from 2024. These measures aim to facilitate the expansion of AI infrastructure while mitigating its strain on the existing power system. As illustrated in Table 1, current regulatory frameworks and policy documents at the EU level span multiple dimensions, including energy efficiency oversight, grid strategic planning and industrial governance for artificial intelligence.

Table 1 Relevant EU Laws, Regulations and Policy Documents on AI and Power Issues

Source: Compiled by the author.

Note: In the table, in force refers to legal texts that have been officially adopted and are currently under implementation; policy framework denotes strategic documents released without direct legally binding effect; under legislative/policy formulation covers measures undergoing public consultation or solicitation of opinions, with no formal legislative proposals or policy frameworks yet issued; voluntary participation refers to non-binding pledges or initiatives launched spontaneously by governmental bodies, industry associations or enterprises, with participation entirely at the discretion of relevant stakeholders.

First, accelerate grid expansion and reform connection rules. Over the past two years, the EU has issued successive forward-looking investment guidelines and efficient grid connection schemes, centering on proactive grid planning based on medium- and long-term demand scenarios, rather than passive expansion triggered merely by project queuing. The upcoming Strategic Roadmap for Digitalisation and AI in the Energy Sector listed in Table 1 reflects this orientation. It integrates data centre grid connection into the overall framework of energy system digitalisation, instead of treating it as an independent infrastructure approval item. Regarding connection regulations, relevant documents from the European Commission explicitly propose preventing speculative applications from locking up grid capacity, raising deposit requirements for retaining connection entitlements, and prioritising projects by maturity rather than application submission date. In regions constrained by grid capacity, non-firm connection and flexible connection have emerged as compromise solutions. Data centres may accept temporary power curtailment under specified conditions in exchange for faster grid access, and scale up gradually through phased commissioning and on-site energy storage, eliminating the need to wait for full grid readiness.

Second, strengthen strategic deployment of nuclear energy and encourage data centres to develop independent microgrids.

In the medium-to-long term, nuclear energy constitutes a critical option for Europe to address surging power demand driven by AI. According to IEA projections, following the commissioning of small modular reactors (SMRs) from 2030 onwards, nuclear power’s share in supplying global data centres is expected to rise further. The European Commission launched the European SMR Industrial Alliance in February 2024, aiming to deploy the first batch of SMRs across Europe in the early 2030s. In October of the same year, the alliance selected nine initial work programmes covering technological routes such as lead-cooled fast reactors, pressurised water reactors and molten salt reactors. Romania is poised to become Europe’s first country to operate an SMR. Meanwhile, self-built power sources and independent microgrids are accounting for an increasing share of data centre power supply. Some data centres bypass lengthy grid connection queues by constructing dedicated power facilities on-site. In March 2026, Dublin commissioned Europe’s first data centre operating entirely on an independent microgrid, enabling full operational autonomy without reliance on the public power grid.

This image shows a nuclear power plant operated by Électricité de France (EDF). At present, only China and Russia have successfully constructed and commissioned small modular reactors (SMRs) worldwide. France has also designated SMRs as a priority pillar within its 2030 nuclear energy investment roadmap, while actively promoting coordinated strategic deployment across the European Union in this field.

Image source: Stephane Mahe / Reuters

Thirdly, enhance the flexibility of the power system. Reforms to the EU electricity market explicitly encourage the adoption of long‑term Power Purchase Agreements (PPAs) and Contracts for Difference (CfDs). These instruments stabilize long‑term power procurement costs, improve the predictability of project financing, and provide a financial foundation for data centres to invest in flexible infrastructure. At the system level, the European Network of Transmission System Operators for Electricity (ENTSO‑E) submitted two policy reform proposals targeting data centres to the European Commission in 2025. The first revises grid connection prioritization rules to allocate capacity based on actual system needs rather than application chronology, granting priority to projects equipped with flexible regulation capabilities. The second establishes incentive mechanisms to engage data centres in grid support services such as frequency regulation and reserve capacity, gradually transforming them from passive power consumers into active adjustable resources for the power grid. Should this transition be realized, it will not only ease grid congestion constraints on data centre expansion but also enable Europe to forge a distinctive competitive edge in global AI infrastructure rivalry—not through sheer power volume, but via superior system efficiency and dispatch capabilities.

Fourthly, curb energy consumption per unit of computing power through energy efficiency standards and sustainability regulations. This approach recognizes that alleviating AI‑driven power pressure requires demand‑side reductions in energy intensity per unit of computation, alongside supply expansion. The EU plans to introduce a comprehensive data centre energy efficiency package encompassing three pillars: the evaluation of submitted operational data, the establishment of a unified data centre rating framework, and the formulation of minimum performance standards. The forthcoming Cloud and AI Development Act directly links streamlined licensing procedures to compliance requirements for energy efficiency, water efficiency, and circularity, with eligibility for policy support contingent on meeting these benchmarks. Member states have introduced even stricter provisions domestically. Germany mandates that all data centres with a load exceeding 300 kilowatts source 100 percent renewable electricity by 2027. Ireland requires newly built data centres to deploy on‑site power generation and energy storage facilities matching their maximum import capacity, alongside participation in wholesale electricity markets to bolster overall system adequacy. In essence, Ireland positions data centres as accountable stakeholders within the power system, rather than mere end consumers.

04 Prospects for Europe’s AI Development under Power Constraints

Fundamentally, Europe faces not merely insufficient power supply, but systemic challenges in industrial coordination. Grid planning, energy transition, data governance, and AI industrial policy are deeply interconnected, necessitating integrated governance within a unified framework rather than fragmented responses. Four key trends will shape future developments.

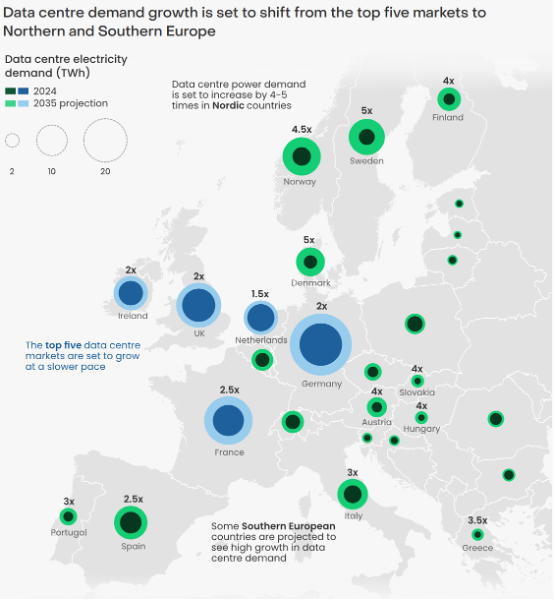

First, the geographical distribution of computing power will become more balanced. Northern, Southern, and selected Eastern European countries with favourable grid access conditions are poised to attract greater investment in new data centres. Meanwhile, traditional Western European core markets including Germany, the Netherlands, and Ireland may see diminished investor appeal amid protracted grid connection backlogs and elevated power prices. This trend will gradually dismantle the current overconcentration of European data centre capacity within the FLAP‑D hubs. According to projections by energy think tank Ember, data centre demand in Northern and Southern Europe will surge by approximately 110 percent by 2030—nearly double the growth rate projected for the five FLAP‑D cities over the same period. By 2035, over half of Europe’s total data centre capacity is expected to be situated outside these established hubs.

Northern Europe stands out prominently. Data centre electricity consumption in Sweden, Norway, and Denmark is forecast to triple by 2030. These nations benefit from limited grid congestion, competitive power prices, low carbon intensity, and cold climatic conditions that reduce energy expenditure for equipment cooling. Critically, their advantages stem from forward‑looking infrastructure planning. Norway’s transmission system operator Statnett has long integrated projected data centre power demand into medium‑ and long‑term grid strategies, reserving capacity for a threefold increase in electricity consumption by 2030. Denmark’s operator Energinet has constructed high‑voltage substations to accommodate data centre loads since 2017, sustaining robust capacity expansion over recent years.

Southern and Eastern Europe likewise demonstrate substantial growth potential. Countries such as Spain, Greece, and Portugal possess abundant land reserves and rich renewable energy resources, positioning them within the expansion roadmaps of major technology corporations. In Eastern Europe, a Warsaw‑centred data centre cluster is emerging in Poland, while Hungary—supported by stable grid conditions—has become an attractive investment destination. Ember estimates that data centre electricity consumption in Austria, Greece, Finland, Hungary, Italy, Portugal, and Slovakia could increase threefold to fivefold between 2024 and 2035.

Northern, Southern and Eastern Europe possess relatively ample grid headroom, offering greater potential for data centre expansion compared with Western Europe.

Image source: Ember

Second, discrepancies may emerge between policy targets and practical capacity. In April 2025, the European Commission released the AI Continent Action Plan, proposing to expand data centre capacity to at least three times its current scale within five to seven years. Nevertheless, authoritative institutions remain cautious over the feasibility of this objective. According to modelling analysis by the IEA, constrained by project delays and grid congestion, Europe’s installed data centre capacity is projected to grow by merely around 70 percent from the 2024 level by 2030—far short of the threefold expansion outlined in the action plan. While France seeks to leverage its nuclear power strengths to attract AI investment, lengthy construction cycles for grid connection and transmission-distribution infrastructure mean its energy advantages cannot be swiftly translated into computing power gains in the short term. Independent forecasts from the IEA, IMF and McKinsey consistently suggest the EU is more likely to double its capacity by 2030, leaving a substantial gap from the tripling target.

Third, the long-term prospects of Europe’s AI industry hinge largely on establishing a viable coexistence pathway between computing expansion and energy transition.

Europe currently faces surging power demand from data centres while navigating a critical phase of industrial electrification, transport electrification and decarbonised heating. Energy consultancy ICIS estimates that incremental power consumption from European data centres will reach approximately 72 terawatt-hours by 2030, comparable to the demand growth from electric vehicles (67 TWh) and industrial electrification (80 TWh). The simultaneous influx of multiple demand streams into an already capacity-strained transmission grid will place unprecedented pressure on power system dispatch and expansion capabilities.

Against this backdrop, compatibility between the EU’s energy transition goals and computing infrastructure expansion will dictate the pace of AI deployment. The revised 2023 Energy Efficiency Directive mandates a minimum 11.7 percent reduction in final energy consumption by 2030 relative to the 2020 baseline projections. The European Commission has also set a target for data centres to achieve carbon neutrality by 2030. In the short term, however, newly installed renewable energy capacity may fail to satisfy both AI expansion and broader electrification needs. IEA projections further indicate that natural gas and coal will still supply over 40 percent of power to global data centres by 2035.

This necessitates pragmatic transitional arrangements in Europe to balance reliable data centre power supply with the phase-out of fossil fuels. Prioritising data centre electricity demand could delay fossil fuel retirement and undermine climate objectives; strictly enforcing energy efficiency and emissions standards, meanwhile, may inflate deployment costs and prolong construction timelines for AI infrastructure. Amid the current political climate and technological rivalry, neither pathway allows for easy deceleration, meaning European policymakers will likely pursue context-specific compromises tailored to individual projects and regions.

Fourth, public attitudes and water resource constraints may pose additional headwinds for Europe’s AI development.

Debates surrounding data centres are extending beyond power supply to intertwined concerns over water intensity and the “social license to operate”. Cooling systems for data centres require massive continuous water intake, while thermal and nuclear power plants supplying their electricity are also major water consumers. The IEA estimates global direct water usage by data centres reached roughly 140 billion litres in 2023. A commentary published in Patterns (Cell Press) notes that when accounting for indirect water intensity from power generation, the total water footprint of AI systems alone could range from 312.5 billion to 764.6 billion litres in 2025. In essence, water pressure for data centres largely represents an extension of power demand pressures.

This tension is particularly acute in water-scarce Southern Europe. Spain’s Aragon region hosts major Amazon data centre clusters yet faces severe drought conditions. In late 2024, Amazon applied to increase water abstraction at three existing Aragon data centres by 48 percent, triggering fierce opposition from local farmers and environmental groups. Activists launched the campaign Tu Nube Seca Mi Río (“Your Cloud Dries My River”), advocating for a moratorium on new data centre construction across Spain.

This image depicts the Monegros Desert in Aragon. The surroundings of Zaragoza, home to Amazon’s data centers, rank among Europe’s most water‑scarce regions, with an average annual precipitation of merely 329 millimeters—comparable to that of Lanzhou in northwestern China. The deployment of large‑scale data centers here has imposed severe pressure on local water resources.

Image source: Wikipedia

Notably, while Northern and Southern Europe are expected to attract greater data center investment, both regions face inherent constraints: Southern Europe grapples with intensifying water scarcity, whereas Northern Europe features a highly environmentally conscious public sensitive to ecological protection. The geographical shift of computing deployment will not necessarily alleviate overall restrictions. This indicates that in Europe, where environmental awareness prevails and regulatory frameworks remain prudential, power supply constitutes only part of the limitations on AI expansion. Water resource pressures and public attitudes will continue to impose sustained constraints on the growth of data center infrastructure.

References

[01] International Energy Agency, Energy and AI, April 10, 2025, https://www.iea.org/reports/energy-and-ai.

[02] International Energy Agency, Electricity 2025: Analysis and forecast to 2027, February 14, 2025, https://www.iea.org/reports/electricity-2025.

[03] International Energy Agency, Electricity Mid-Year Update 2025, July 30, 2025, https://www.iea.org/reports/electricity-mid-year-update-2025.

[04] OPEC, World Oil Outlook 2050 (WOO 2025), July 10, 2025, https://www.opec.org/assets/assetdb/woo-2025.pdf.

[05] European Commission, The AI Continent Action Plan, April 9, 2025, https://digital-strategy.ec.europa.eu/en/library/ai-continent-action-plan.

[06] European Commission, An EU Action Plan for Grids, November 28, 2023, https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX%3A52023DC0757.

[07] European Commission, Guidance on Efficient and Timely Grid Connections, December 10, 2025, https://energy.ec.europa.eu/document/download/62c46b3d-0df9-42a1-a5fe-c3c71ed5f18c_en?filename=C_2025_8473_1_EN_ACT_part1_v4.pdf.

[08] European Commission, Energy Efficiency Directive, https://energy.ec.europa.eu/topics/energy-efficiency/energy-efficiency-targets-directive-and-rules/energy-efficiency-directive_en.

[09] European Commission, “In Focus: Data Centres – An Energy-Hungry Challenge,” November 17, 2025, https://energy.ec.europa.eu/news/focus-data-centres-energy-hungry-challenge-2025-11-17_en.

[10] European Commission, “Energy Performance of Data Centres,” https://energy.ec.europa.eu/topics/energy-efficiency/energy-efficiency-targets-directive-and-rules/energy-efficiency-directive/energy-performance-data-centres_en.

[11] European Commission, “New Impetus for Energy Efficiency,” https://energy.ec.europa.eu/topics/energy-efficiency/new-impetus-energy-efficiency_en#deliverables-2025-2026.

[12] European Commission, “European Industrial Alliance on SMRs,” https://single-market-economy.ec.europa.eu/industry/industrial-alliances/european-industrial-alliance-small-modular-reactors_en.

[13] European Commission, “Electricity market design,” https://energy.ec.europa.eu/topics/markets-and-consumers/electricity-market-design_en.

[14] ACER, 2025 Monitoring Report on Cross-Zonal Electricity Trade and Congestion Management, https://www.acer.europa.eu/sites/default/files/documents/Publications/ACER-Monitoring-Report-2025-crosszonal-electricity-trade-capacities.pdf.

[15] Congressional Research Service, “Data Centers and Their Energy Consumption: Frequently Asked Questions,” January 23, 2026, https://www.congress.gov/crs-product/R48646.

[16] Irish Commission for Regulation of Utilities (CRU), Large Energy Users Connection Policy, December 12, 2025, https://cruie-live-96ca64acab2247eca8a850a7e54b-5b34f62.divio-media.com/documents/CRU2025236_Large_Energy_User_connection_policy_decision_paper.pdf.

[17] Arman Shehabi et al., 2024 United States Data Center Energy Usage Report, Lawrence Berkeley National Laboratory, December 2024, https://eta-publications.lbl.gov/sites/default/files/2024-12/lbnl-2024-united-states-data-center-energy-usage-report.pdf.

[18] Goldman Sachs, “Powering the AI Era,” July 2025, https://www.goldmansachs.com/what-we-do/investment-banking/insights/articles/powering-the-ai-era/report.pdf.

[19] Matteo Mazzoni et al., “Data centres: Hungry for power,” ICIS, https://www.icis.com/explore/resources/data-centres-hungry-for-power/.

[20] Christian Bogmans et al., “Power Hungry: How AI Will Drive Energy Demand,” IMF, April 22, 2025, https://www.imf.org/-/media/files/publications/wp/2025/english/wpiea2025081-print-pdf.pdf.

[21] Christian Bogmans et al., “AI Needs More Abundant Power Supplies to Keep Driving Economic Growth,” IMF Blog, May 13, 2025, https://www.imf.org/en/Blogs/Articles/2025/05/13/ai-needs-more-abundant-power-supplies-to-keep-driving-economic-growth.

[22] James O’Donnell and Casey Crownhart, “We Did the Math on AI’s Energy Footprint. Here's the Story You Haven’t Heard,” MIT Technology Review, May 20, 2025, https://www.technologyreview.com/2025/05/20/1116327/ai-energy-usage-climate-footprint-big-tech/.

[23] Adam Zewe, “Explained: Generative AI’s Environmental Impact,” MIT News, January 17, 2025, https://news.mit.edu/2025/explained-generative-ai-environmental-impact-0117.

[24] Jesse Noffsinger et al., “The cost of compute: A $7 trillion race to scale data centers,” McKinsey, April 28, 2025, https://www.mckinsey.com/industries/technology-media-and-telecommunications/our-insights/the-cost-of-compute-a-7-trillion-dollar-race-to-scale-data-centers.

[25] Anna Granskog et al., “The role of power in unlocking the European AI revolution,” McKinsey, October 24, 2024, https://www.mckinsey.com/industries/electric-power-and-natural-gas/our-insights/the-role-of-power-in-unlocking-the-european-ai-revolution.

[26] Erikhans Kok et al., “Scaling bigger, faster, cheaper data centers with smarter designs,” McKinsey, August 1, 2025, https://www.mckinsey.com/industries/private-capital/our-insights/scaling-bigger-faster-cheaper-data-centers-with-smarter-designs.

[27] Elisabeth Cremona et al., “Grids for Data Centres: Ambitious Grid Planning Can Win Europe's AI Race,” Ember, June 19, 2025, https://ember-energy.org/latest-insights/grids-for-data-centres-ambitious-grid-planning-can-win-europes-ai-race/.

[28] Duncan Stewart et al., “Why AI’s next phase will likely demand more computational power, not less,” Deloitte, November 18, 2025, https://www.deloitte.com/us/en/insights/industry/technology/technology-media-and-telecom-predictions/2026/compute-power-ai.html.

[29] “Newly added US data center capacity slows down considerably in Q4 2025, as market struggles to keep up with explosive demand,” Wood Mackenzie, March 16, 2026, https://www.woodmac.com/press-releases/newly-added-us-data-center-capacity-slows-down-considerably-in-q4-2025-as-market-struggles-to-keep-up-with-explosive-demand/.

[30] Matt G. O’Neill, “Data Centres in Ireland: The State of Play,” The Institute of International and European Affairs, December 18, 2025, https://www.iiea.com/blog/data-centres-in-ireland-the-state-of-play.

[31] Rebecca Leppert, “What we know about energy use at U.S. data centers amid the AI boom,” Pew Research Center, October 24, 2025, https://www.pewresearch.org/short-reads/2025/10/24/what-we-know-about-energy-use-at-us-data-centers-amid-the-ai-boom/.

[32] Josh Gabbatiss, “AI: Five Charts That Put Data-Centre Energy Use – and Emissions – into Context,” Carbon Brief, September 17, 2025, https://www.carbonbrief.org/ai-five-charts-that-put-data-centre-energy-use-and-emissions-into-context/.

[33] Alex de Vries-Gao, “The Carbon and Water Footprints of Data Centers and What This Could Mean for Artificial Intelligence,” Patterns, Vol. 7, No. 1, Published Online, https://www.cell.com/patterns/fulltext/S2666-3899(25)00278-8.

[34] Sophia Akram, “Elon Musk at Davos 2026: why technology could shape a more ‘abundant future’,” World Economic Forum, January 24, 2026, https://www.weforum.org/stories/2026/01/elon-musk-technology-abundant-future-davos-2026/.

[35] Maximilian Henning, “EU’s flagship tech sovereignty package delayed again,” Euractiv, March 17, 2026, https://www.euractiv.com/news/eus-flagship-tech-sovereignty-package-delayed-again/.

[36] Lucy Raitano, “Power supply constraints slowing EMEA data centre rollout, report says,” Reuters, November 7, 2025, https://www.reuters.com/business/energy/power-supply-constraints-slowing-emea-data-centre-rollout-report-says-2025-11-06/.

[37] Laila Kearney, “Google Expands Utility Deals to Curb Data-Center Power Use during Peak Demand,” Reuters, March 19, 2026, https://www.reuters.com/sustainability/boards-policy-regulation/google-expands-utility-deals-curb-datacenter-power-use-during-peak-demand-2026-03-19/.

[38] Alban Kacher, “Belgium mulls energy limits for power-hungry data centres as AI demand surges,” Reuters, October 23, 2025, https://www.reuters.com/business/energy/belgium-mulls-energy-limits-power-hungry-data-centres-ai-demand-surges-2025-10-22/.

[39] “France to harness nuclear power for AI data centres, says Macron,” Reuters, March 10, 2026, https://www.reuters.com/business/energy/france-harness-nuclear-power-ai-data-centres-says-macron-2026-03-10/.

[40] “US needs more energy development to power AI, Google president says,” Reuters, March 23, 2026, https://www.reuters.com/business/energy/ceraweek-us-needs-more-energy-development-power-ai-google-president-says-2026-03-23/.

[41] John Ainger, “EU Will Work on Setting Water Use Caps for Thirsty Data Centers,” Bloomberg, May 15, 2025, https://www.bloomberg.com/news/articles/2025-05-15/eu-will-work-on-setting-water-use-caps-for-thirsty-data-centers.

[42] Luke Barratt et al., “Revealed: Big tech’s new datacentres will take water from the world’s driest areas,” The Guardian, April 9, 2025, https://www.theguardian.com/environment/2025/apr/09/big-tech-datacentres-water.

[43] April Roach and Gaelle Legrand, “Powering AI: Europe switches on its first microgrid-connected data center,” CNBC, March 11, 2026, https://www.cnbc.com/2026/03/11/data-center-microgrid-power-ireland-ai-boom-avk-pure-dc.html.

Authors

Huang Kaiyue, Research Assistant of CGAIG

Yao Xu, Secretary-General of CGAIG and Associate Professor at FDDI